Ferrari (NYSE:RACE) is Recession Proof – Live Trading News

#Ferrari #RecessionProof

$RACE

Ferrari (NYSE:RACE) is a story of racing prestige, wealth plus exclusivity around its brand since its introduction in Y 1947.

Ferraris are expensive, the average selling price of just over $324,000 in Y 2019.

Ferrari is not a typical car maker, the Maranello Outfit built its business model for success in any market condition.

Becoming a new Ferrari owner is difficult and almost always requires proof of prior ownership.

In order to buy a new Ferrari, customers must demonstrate that they have owned at least 1 new or preowned Ferrari in the past. This makes the cars’ secondary market strong.

And there is the Ferrari owners club. Members get invited to super events around the world. These events offer networking opportunities for any clienti invited. Wealthy people from all over the world travel to Ferrari’s HQ in Maranello to bespoke their new cars and pay their money in exchange.

Enzo Ferrari was a racing driver for Alfa Romeo, he was obsessed with racing. He formed his own team called Scuderia Ferrari, which still exists today. His obsession with racing never ended. He began building his own Ferrari-badged cars and winning high profile races across Europe and America.

Enzo focused on building winning race cars, and his production was limited. So Ferrari produced a small number of cars available to the public each yr. This made Ferrari cars exclusive, leaving buyers waiting in line for their opportunity to buy 1.

During Ferrari’s Q-1 Y 2020 conference call CEO Louis Camilleri stated that its order book extends “well beyond 12 months.” Customers are waiting more than a year to buy. If that opportunity presents itself and the customer decides not to purchase, there is long line to fill the slot.

The Big Q: What does it mean for shareholders?

The Big A: as follows;

Ferrari trades at 65X trailing-12-month net income because the firm has remarkable pricing power.

Over the last 7 yrs, Ferrari’s gross margins steadily increased from 47% to 52%. At Ferrari the average cost of production per car — cost of sales divided by unit shipments — rose just 1% from Y 2013 to Y 2019, even as the number of vehicles cars shipped annually rose nearly 45% over the frame. This demonstrate to investors that Ferrari owes its margin expansion to the underlying pricing power of its business model.

Clienti, are willing to pay more, but some analysts believe that in many cases, customers also like to pay more. Since production costs have stayed flat, this pricing power has trickled to the bottom line. From Y 2013 to Y 2019, EBIT margins grew from 15.6% to 24.4%, and net income margins from 10.3% to 18.5%.

Ferrari’s Key objective is making sure demand steadily outpaces supply. In order to do that, its brand is very important.

The best indicator of brand value is Ferrari’s customer backlog.

CEO Louis Camilleri talks about this metric on every conference call, and for the last few years, the backlog has stayed consistent at longer than 12 months. So, as long as Ferrari maintains a strong backlog and no sign of brand erosion, the company should continue to increase profits at a sustainable rate.

Ferrari is The Aristocrat of the automotive sector.

Enzo Ferrari’s iconic Italian Supercar manufacturer claimed the title according to the latest Brand Finance Global 500 2019 report launched at the World Economic Forum in Davos

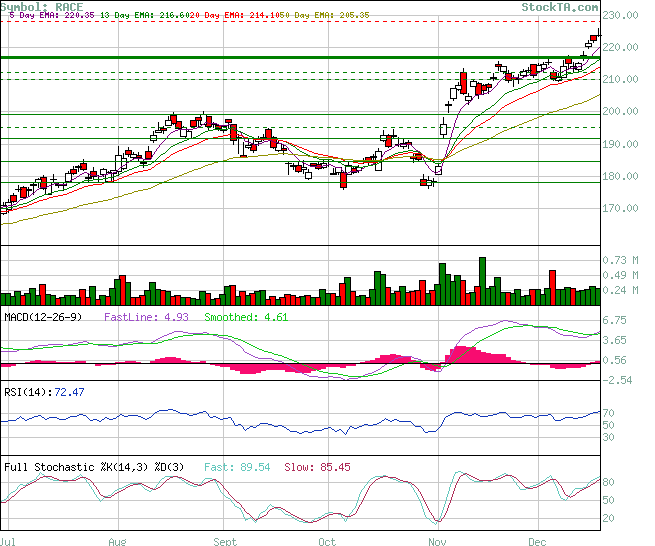

HeffX-LTN overall technical outlook for RACE is overall Very Bullish, the Key resistance is at, the Key support is at .

Our overall technical outlook is Very Bullish, a Key indicators are Bullish long-term. Ferrari reported strong earnings for Q-3 on 3 November.

Ferrari finished trading Wednesday at 212.39 in NY. It’s all time high was marked at 215.48 marked intraday Wednesday, 18 November.

All technical indicators are Very Bullish there is Strong support at 199.16, there is no overhead resistance.

The Maranello Outfit’s shares were raised to Buy from Hold at HSBC, Morgan Stanley and Bank of America. UBS is now calling the stock at 365.

Ferrari will continue to create value in the long term as it becomes the world’s 1st Super Luxury brand.

Ferrari is a quality 1st long term luxury products investment, BAML raised it call to 270 long term.

I have raised my long term target to 375, a Strong Bull call, the strongest on the Street.

Ferrari has an average rating of Buy and a consensus target price at 211.95.

The Maranello Outfit’s shares were raised to Buy from Hold at HSBC.

Ferrari will continue to create value in the long term. Ferrari is a quality 1st long term luxury products investment, and I am calling it 375 long term , the Top on the Street, and adjusting it to 230/share short term.

A number of large investors have recently bought shares of RACE. And there is no insider selling.

The stock is now considered defensive in the sector.

Have a healthy day, Keep the Faith!

.